Chapter 3: Challenges and complexities

In this chapter, we outline the challenges and complexities that prevent councils from building more housing. These range from financial and legal issues to politics and development capacity.

Finance

Access to finance to build more housing is a key challenge for councils, with interviewees citing “artificial government restrictions” on funding.

Right to Buy receipts

Investment in affordable homes through the use of RTB receipts has proved to be a challenge. Receipts can only provide 30 per cent of the costs of a replacement home, and must be used within three years before funds are passed to HM Treasury (and then the GLA). 40 This leaves councils with short timescales to put together a funding package, secure planning, appoint contractors, and commence construction. As sales of former council properties are rapidly increasing, boroughs struggle to find the remaining funds within their balance sheets, meaning that the GLA has received more than £50 million in unspent RTB receipts from councils since 2012. 41 A new initiative announced by the Mayor of London in May 2018 will allow receipts to be passed by boroughs to the GLA, and ring-fenced for investment in affordable housing by the same councils. 42 Further, the government recently announced a consultation on the flexibility of RTB receipts as part of the upcoming Social Housing Green Paper. 43

Borrowing capacity

Borrowing through the Housing Revenue Account is heavily constrained (see following page), and only around seven London boroughs have both regular revenue from council-owned housing stock (which can be borrowed against) and the headroom required to take advantage of HRA borrowing. 44 The lack of borrowing capacity and flexibility hampers some councils’ housebuilding efforts in the medium-term, more councils are set to reach their headroom capacity, though government has announced that half of the £1 billion borrowing cap raise will go to London. This is often the driver behind setting up a wholly-owned company to enable financing from outside the HRA that can support mixed market and affordable housing – or entering into joint ventures with partners who have better access to finance.

HRA headroom

As outlined in previous research undertaken by Centre for London on affordable housing in London, 45 some councils have been undertaking housebuilding through borrowing on the Housing Revenue Account (HRA) – a primary means of funding local authority housebuilding programmes. HRAs hold the income and expenditure relating to council-owned housing, and this income is ring-fenced so that it can only be spent on local affordable housing provision.

In 2012, the government introduced the self-financing regime, which meant that any gap between income and projected spending would now be covered by

borrowing rather than national government subsidy, and that the amount that local authorities can borrow is capped by local finance regulations. A council’s capacity to borrow through the HRA is thus dependent on there being a gap, or “headroom”, between historic debt levels and agreed borrowing capacity, rather than on more conventional criteria such as the authority’s ability to service the debt (which applies to prudential borrowing).

46

As a result, there is a large variation in the amount of headroom between boroughs, which ranges from zero in Harrow to £148m in Lambeth. In 2012 only around seven London boroughs had both regular revenue from council-owned housing stock (which can be borrowed against) and the headroom required to take advantage of HRA borrowing. 47

Legislative and regulatory issues

Legal and taxation issues emerged during interviews as a barrier to setting up wholly-owned companies, with different legal advisors advising boroughs in different ways and sometimes discouraging councils from setting up companies. There was a perceived lack of clarity in the process of setting up a wholly-owned company, and some boroughs argued that setting up a company represents a significant cost in terms of time and finance which isn’t justified by the scale of their programme.

Although setting up a wholly-owned company can be complex, it can also generate revenue in the long term, and several councils have set up a company for future development. The complexities of setting up a company from scratch have encouraged some councils to use an existing ALMO to undertake development in the first place, although this arrangement may not be as flexible to future changes and may come with financial and tax constraints. 48

Intra-council issues

Politics

Political leadership seems key to enabling council-led delivery. Politicians can increase confidence locally and garner support from different teams across the council, but local politics can also hamper delivery – for instance, when constituents oppose development for a number of reasons. 49 Some interviewees also observed that local political support can itself be problematic if it tips over into micromanagement. Wholly owned council companies have governance outside formal council structures, and may be more resilient to political cycles – although many are still in their infancy and have yet to face significant political change.

Finance and housing teams

Interviewees suggested that the enthusiasm of housing and regeneration teams for investing in council-led delivery is not always shared by finance teams, who may take a more risk-averse approach. Other research has shown that in some cases, local authority housing officers do not want to establish housing companies, because they think this will lead to a loss of control. 50 The challenge of securing “buy-in” across the council serves to underline the importance of clear political and managerial leadership.

Capacity and expertise

Attracting and retaining the right staff is a challenge for councils, which often offer lower salaries than the private sector does for equivalent roles. Several councils have managed to build in-house teams, attracting staff for whom working for a public purpose is a strong motivator. Councils are also working with freelancers (in long-term appointments) with expertise in project management and deal-making. Design and other professional services are generally commissioned from consultant teams, though some councils are building their own in-house architectural and urban design teams, both for direct delivery – such as Islington (Islington Architects) and Hackney – and as part of wholly-owned companies (for example, Brick by Brick).

Planning and development issues

As councils increasingly act as developers, they face developer issues – such as the lack of land in some boroughs or sites that are difficult to unlock. Many councils, even when undertaking development in-house, are encountering barriers to affordable housing delivery such as a scarcity of brownfield sites and escalating land values. 44

Another issue is the ability to find contractors. This is an issue for all developers but is especially challenging for infill sites, where much council-led delivery is focused.

Cuts have also affected capacity: budgets for planning and development fell by almost 50 per cent per capita between 2010 and 2018, the steepest reduction of all service areas in London. 52

In addition, going through the planning process can be challenging when the council is the applicant. Councils face much more upfront local opposition – sometimes driven by suspicion about the relationship between development and planning functions – and have a brighter spotlight shone on their planning commitments and policy adherence.

Risk

A market slowdown could affect the business case for council-led approaches, particularly cross-subsidy models, which depend on buoyant private sales. Councils’ risk exposure increases – alongside potential benefits – when they undertake development themselves, rather than simply selling land. However, councils also retain their assets and can put in place policies and procedures to assess and respond to the level of risk. Councils have developed a number of exit or mitigation strategies, including switching tenure mix (for example, from sale to rental), seeking alternative sources of funding, or adopting an altered timeline.

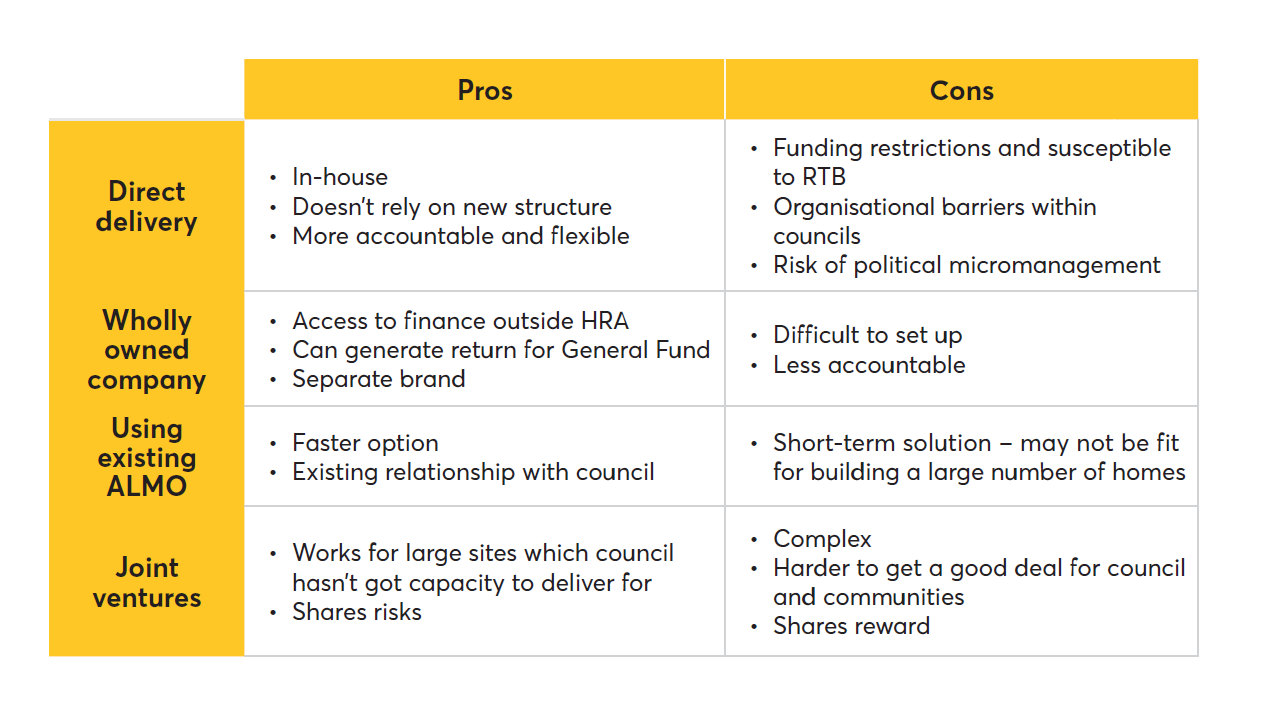

The range of approaches taken by councils

The challenges outlined in this chapter are hampering both the speed and the quality of development, meaning council housebuilding is not fully realising its potential. What emerges from this analysis of barriers is that different councils use different vehicles to deliver new housing, depending on local circumstances, needs and cultures. Some interviewees felt that company structures offered the opportunity to operate entrepreneurially; others felt that they were an awkward “fix” of the broader barriers to council housebuilding. But some common challenges – those of financing, capacity and political leadership – apply in most if not all cases. Nonetheless, our research indicates that to date, 21 boroughs have set up a wholly-owned development company (16 of which are active), and 14 boroughs are building new homes through direct delivery. In total,

22 boroughs have homes in the pipeline through active council-led delivery models. Although there are pros and cons to each option – as outlined in the table below – it seems that with political will and vision, boroughs can play a bigger role in delivering housing locally, retain a longer-term stake in the development of their areas, and make the most of their existing assets.