Chapter 3: Sector analysis

In this chapter, we review existing evidence and draw on our primary qualitative research with sector experts. This enables us to give a snapshot of giving patterns and trends

across our five “giving sectors”:

a) Trusts and foundations: grant-making by independent foundations and family/community trusts; wider “funder plus” activity such as campaigning and influencing; and voluntary sector capacity building.

b) General Public: charitable donations and volunteering from individuals.

c) High Net Worth (HNW) individuals: donating and in-kind support from wealthy individuals (predominantly those with over £1m in investable wealth).

d) Corporates: corporate fundraising, corporate social responsibility (CSR) activity, and employee giving and volunteering.

e) Social investors: social and impact investing from individuals, foundations, corporates, and social investment intermediaries.

For each of our sectors, we provide an overview, bringing together available data on the level and distribution of giving as well as relevant trends. We identify important actors, describe the institutional makeup of each sector, and provide case studies on innovative practice in the capital and internationally. We start with trusts and foundations, as they play an outsized role – not so much in the amount they give, but in their support for London’s giving infrastructure and other vital strategic initiatives.

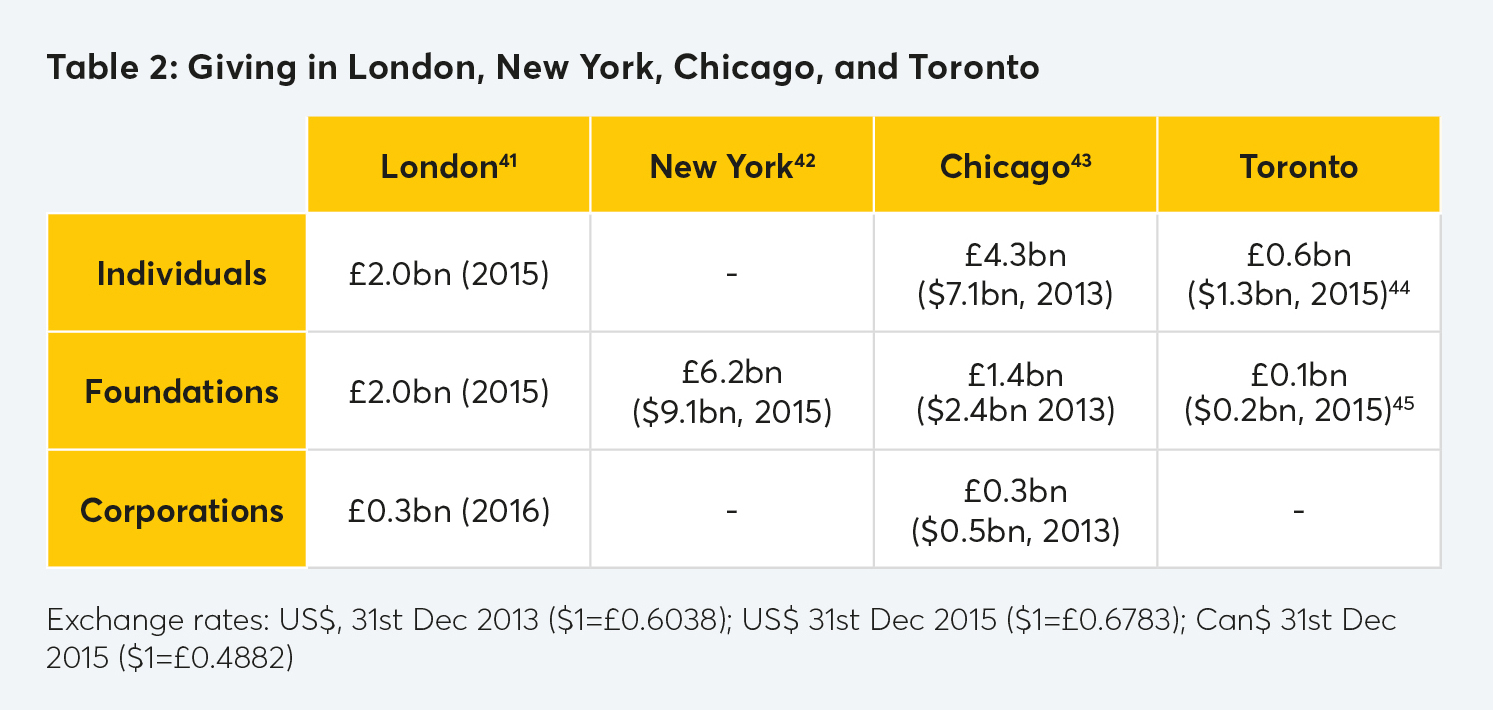

How does London compare to other global cities?

Definitional and methodological differences make it difficult to draw robust like-for-like comparisons with research into giving in other major cities, but available studies do provide broad benchmarks for levels of giving in London. Data is, however, extremely patchy, and this project was unable to find comprehensive statistics across all five “giving sectors” for any other major global city. The best evidence comes from a number of studies and publicly available datasets reviewing levels of giving by individuals, trusts and foundations, and/or corporates in New York, Chicago, and Toronto.

41: Pharaoh, C., & Walker, C. (2015). More to Give. London: City Philanthropy Trust.

42: See Foundation Centre (2018). Retrieved from: https://maps. foundationcenter.org.

43:The Chicago Community Trust (2018). Giving in Chicago. Retrieved from: http://givinginchicago.com.

44: Canada Helps (2017). The Giving Report 2017. Retrieved from: https://www.canadahelps.org/en/the-giving-report/ download-the-report.

45: See Foundation Centre (2018). Retrieved from: https://maps. foundationcenter.org.

Perhaps unsurprisingly, these figures suggest that London is outperformed by some of the major US cities (New York on grant-making, and Chicago on individual giving). The differentials are, however, possibly less than we would expect based on national-level statistics showing that in 2015 Americans gave $258.5bn to charity (1.4 per cent of GDP), compared to $17.4bn in the UK (0.5 per cent of GDP). 39

With its strong giving culture, the US is often a source of inspiration for those interested in growing philanthropy in the UK. But while there is much to learn from the US, we are not going to boost giving in London without understanding what is distinctive about its particular strengths and weaknesses. Charities Aid Foundation’s (CAF) Rhodri Davies argues that:

“It seems neither feasible nor desirable to try and replicate exactly the US system and culture of giving here in the UK [and while] we can […] use the top line figures as a benchmark for where we would like levels of giving in the UK to be, our ambition should be to achieve this goal through developing a uniquely British giving culture”. 40

a. Trusts and foundations

Sector overview

London is the national capital for independent grantmaking trusts, with 11 out of the country’s 20 biggest trusts and foundations based in the city. 41 In total, 61 per cent of the UK’s largest 300 independent foundations are headquartered in London. 42 Analysis commissioned for this project, conducted by the Directory of Social Change (DSC), finds a total grant spend by all Londonbased grant-makers of £2.04bn in 2016, equivalent to 31 per cent of all grant spending in the UK. 43 Much of this funding flows outside of the capital to other parts of the UK and internationally, with the DSC analysis estimating that £600 million (or 29 per cent) was retained within the capital in 2016. National-level funders are supported by a range of advisory and infrastructure organisations also located in the capital, including membership bodies – such as the Association of Charitable Foundations (ACF) and National Council for Voluntary Organisations (NCVO) – and research and advisory organisations such as New Philanthropy Capital (NPC) and the Institute for Voluntary Action Research (IVAR). London’s trust and foundation ecosystem is complex and multi-layered, with huge national and international foundations like the Wellcome Trust (which alone accounts for over 10 per cent of all UK grant spending) 42 sitting alongside more locally focused funders. London’s reputation as a “centre of global civil society” is at least in part a result of its concentration of international development foundations. 45 All 10 of the UK’s largest internationally focused foundations are based in the capital, with the most recent estimates putting annual grants from these organisations at £171m per year. 46 These organisations are again supported by a strong London-based infrastructure, including Bond, the national membership body for international development charities. They also benefit from proximity to the Department for International Development (DFID), which oversees the 0.7 per cent of UK gross national income spent on foreign aid. 47

London-focused funders

While most large national funders make grants to London, there are also a large number of independent foundations focusing exclusively on addressing need within the capital. These can be segmented in a number of ways, including by their geographical area of benefit – dividing into large pan-London funders such as City Bridge Trust, Trust for London and the London Community Foundation (established in its present form only in 2012, from the merging of various local foundations), multi-borough funders like John Lyon’s Charity, and single-borough funders such as the Cripplegate Foundation. In the latter category, while most boroughs will have some kind of localised community fund (often administered by the London Community Foundation), the distribution of larger single-borough funders is highly uneven, with only four boroughs – Islington, Lambeth, Kensington, and Richmond – having dedicated funders making annual grants of over £1m (see Table 5).

London’s philanthropic history can be traced in many of the names of its national (e.g. Henry Smith) and London-level funders (e.g. John Lyon and Edmund Walcot), as well as the charitable activities of the City’s 110 livery companies. 48 While funding activity from many of the liveries is small or directed solely at one institution, a number – particularly the Clothworkers, Mercers, and Goldsmiths – operate sizeable open grant programmes and function much like other independent grantmakers. These grant programmes, while often weighted towards London, also have national reach. While most London-focused funders make grants from their own endowments, London’s two community foundations – London Community Foundation and East End Community Foundation – manage other endowments and also develop new grant programmes through active fundraising from business and individuals.

56: List derived from personal communication, Directory of Social Change; funding figures from Pharaoh, C., Walker, C., & Goddard, K. (2017). Giving Trends 2017: Top 300 Foundation Grant-Makers. London: Association of Charitable Foundations.

As well as support from national-level infrastructure, London’s funder ecosystem is connected by a number of London-specific networks. At a pan-London level, London Funders convenes over 100 public and private funders based in the capital – predominantly foundations and local authority grant-makers, but also corporate funders and advisory organisations. Funders have an opportunity to meet throughout the year through a number of thematic (e.g. Children and Young People) and practise-based (e.g. Measurement and Evaluation) network groups. There are also networks emerging at a more local level, such as Lambeth Funders Forum, which brings together local funders like the Walcot Foundation, Battersea Power Station Foundation, and Guy’s and St Thomas’ Charity.

Key trends in giving by trusts and foundations

The distribution of grant funding in London

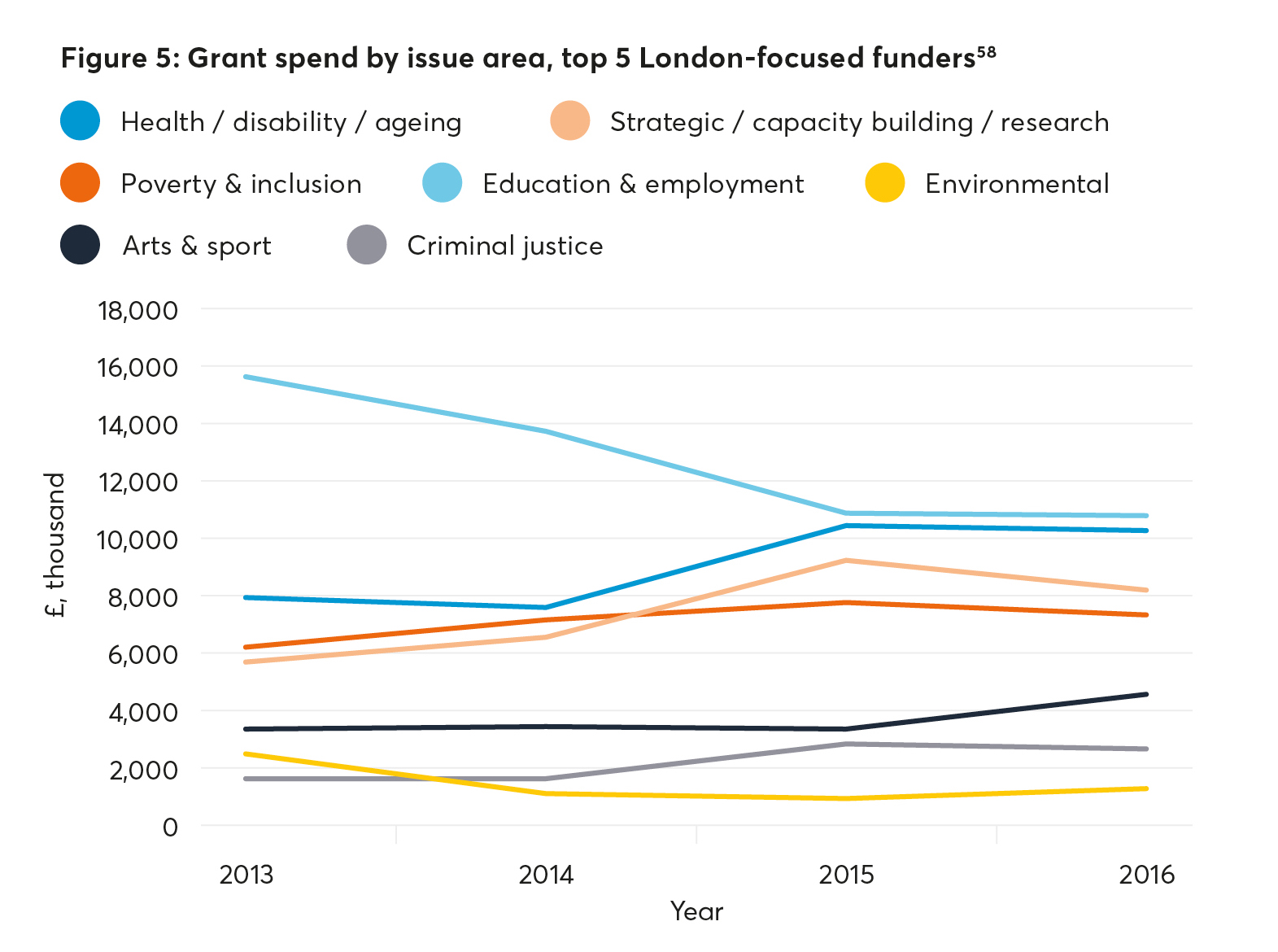

No comprehensive aggregate statistics currently exist on the causes funded by independent foundations in the capital (although progress on this is being made through the 360Giving initiative). Taking a sample of the top five London-focused funders by grant spend, we can see that education/employment and health-related causes are the most commonly funded causes – accounting for 24 and 23 per cent of funding respectively in 2016 (see Figure 5). Over the last four years, funding from our sample has risen for health whilst falling for education and employment. This is in part due to additional funds made available by the City of London Corporation to City Bridge Trust to tackle unemployment in the wake of the “Great Recession” coming to an end, together with a growth in mental health funding from City Bridge and a new partnership between The London Community Foundation and a borough Clinical Commissioning Group (CCG).

We have also seen a rise in “strategic” funding – not necessarily tied to a specific cause, but instead focused on what is sometimes called “funder plus” activity, including direct capacity-building support with grantees and wider campaigning and influencing work. This includes Trust for London’s longstanding funding of the London Poverty Profile – which since 2009 has provided a detailed borough-by-borough analysis of trends linked to poverty and disadvantage – and City Bridge Trust’s strategic initiative to “embed a culture of philanthropy” across the City and the wider capital. 49

Funder collaboration: an intensification of joint working in response to austerity

58: Centre for London analysis, using data from foundation annual reports.

Another important trend has been a move towards greater coordination and collaboration among trusts and foundations.

“Whereas 10 years ago maybe you could still plough your own furrow and just go down one grant stream or one commissioning stream […] now you have to collaborate if you’re going to achieve impact.”

Director, infrastructure organisation

Austerity has undoubtedly been a significant factor in catalysing the collaborative ethos among trusts and foundations. One expert interviewee spoke about “austerity in effect forc[ing] collaboration onto us”, with independent funders seeing collaboration as a route to addressing emerging funding gaps. Collaboration has also been “forced on” funders as a result of a need to gather together all available resources in responding to moments of crisis, particularly around recent terror attacks and the Grenfell Tower tragedy (see Case Study 1). That said, there is also a growing recognition across the sector that entrenched social problems can only be effectively tackled through collaboration:

“[There’s a growing] recognition that complex problems require complex systemic solutions, and no one institution, or one category of institution, has all that is required to change the system.”

Independent consultant

Collaborative initiatives include Moving On Up, a £1m project to increase the employment rates for young black men in London, funded jointly since 2014 by the two largest pan-London foundations (City Bridge Trust and Trust for London). There have also been joint funding programmes between pan-London and borough-level funders, including City Bridge Trust and Cripplegate Foundation’s funding of the Islington Giving initiative from 2010; and a partnership between Trust for London and the Walcot Foundation, supporting in-work progression for low-income groups in Lambeth from 2015.

While there has traditionally been some reluctance around joint working between the local public sector and private funders, this is also changing, aided in part by the cross-sector networks cultivated by the likes of London Funders. Collaboration in this context is driven by the necessities of much-reduced local authority budgets, but also by a shift to more place-based approaches from foundations. As NLGN points out, a renewed focus on place by independent funders means that they can often “find councils to be strong partners who can help them to rethink their investment programmes in line with place-based priorities, with rich data on local need”. 50 Concrete collaborative projects are beginning to emerge, including joint funding between John Lyon’s Charity and local authorities in Camden, Westminster, and Hammersmith and Fulham around youth service provision (see Case Study 2).

Case Study 1: The funder response to the Grenfell Tower fire

The tragedy of the Grenfell Tower fire in June 2017 triggered a huge giving response from Londoners and people across the country. It also mobilised large parts of London’s civil society, including community groups, faith groups, large national charities, and local, national, and international funders. Developing a coordinated response was a huge challenge, for funders, given the scale and the immediacy of need, the level of donations from the general public, and the intense media scrutiny that accompanied the fundraising effort.

The funder response to Grenfell falls into two broad areas. First, there were funders who, with other NGOs, helped coordinate the distribution of funds raised by the general public to the victims and their families. Second, there was also funder collaboration around the provision of grant funding to local community organisations.

In the first category, three major fundraising campaigns were set up in the immediate wake of the incident:

-

Evening Standard and London Community Foundation Dispossessed Fund, which had raised £6.8m by 25th January 2018. 51

-

British Red Cross and London Emergencies Trust fund, which has raised £7.2m.

-

Kensington and Chelsea Foundation, which has raised £6.8m.

In the second category, London Funders helped to convene relevant foundations and public funders by setting up a number of specific funds targeting support to local community organisations. John Lyon’s Charity led two of these funds – dedicated to providing grants to organisations supporting young people in the area – while other funding programmes were set up to fund the core costs of community groups, and for organisations providing legal and financial advice to survivors.

All of the funds were developed through matched funding by a range of different public and private funders, and enabled by an online portal set up by London Funders. The portal allowed one single application point for all community groups in need of funding. It also provided a forum to bring together grant managers from each of the supporting funders, who would make collective decisions about which grant-makers would be best placed to fund individual applicants. In the case of the John Lyon’s-led funds, this received matched funding from Big Lottery Fund, the Tudor Trust, City Bridge Trust, and the Department for Education, among others. In total, £2.3m was distributed to local community organisations. 52

Both sets of funders faced significant challenges. Those supporting local community organisations had to rapidly come together to establish a single application form something that had been discussed for many years in London but never developed. For those distributing fundraised income, there were initial problems identifying victims, and there has been criticism around the duplication of campaigns and the speed at which money reached victims and families. 53 However, in incredibly difficult circumstances, each of these campaigns had allocated over 80 per cent of fundraised income to distributing organisations by January 2018. London Emergencies Trust has now made payments of between £3,500 and £30,000 to those hospitalised, as well as £100,000 to bereaved next of kin. 54

Case Study 2: Young People’s Foundations

John Lyon’s Charity (JLC), which makes grants to charities working with young people across eight London boroughs and the City, has over the past three years established a new collaborative funding model in response to large cuts in local authority funding for youth services.

Beginning in Brent in 2014, where the council had announced a 75 per cent cut in funding for youth services, JLC worked to convene local youth organisations to pool expertise, build resilience, and develop a more sustainable collective funding model. Young Brent Foundation was established in 2015, along with the Young Barnet Foundation and Young Harrow Foundation, with core funding provided by JLC and City Bridge Trust. Since then, four more Young People Foundations (YPFs) have been established, three of which (Westminster, Camden, and Hammersmith & Fulham) have been co-funded by the local authority. The YPFs operate as membership organisations which provide five core

functions:

-

Acting as a prime contractor at a local level. This involves building consortia among the membership, and applying for grants or contract incomes as a single entity.

- Running local network groups. This includes issue- and locality-based groups to enable the sharing of expertise, and the delivery of capacity building support.

-

Operating a small grants scheme. This local funding pot is aimed particularly at smaller organisations such as youth clubs that may not be able to engage in consortia bidding.

-

Creating an online “venue bank”. This will enable members to share space, and match need for venue space with spare capacity.

-

Acting as a single point of contact to pull in other philanthropic support. This will establish a brand and single access point, particularly for corporates looking to provide financial and in-kind support to youth organisations in the borough.

Following the initial set-up phase, the YPFs have begun to bring in new funding streams. Young Barnet Foundation was, for example, successful in securing funding as part of the National Citizenship Service Pathfinder programme. Young Westminster Foundation has secured funding from a number of corporate partners – and other foundations have been given venue space by businesses through the new venue bank system.

Strategic projects and “funder plus”: innovation to transform the funding landscape

As public spending cuts transform the funding landscape, trusts and foundations are increasingly recognising their influence and responsibilities in creating a supportive funding environment. This is in part about changing grant-making practices in response to the needs of grantees around core funding and capacity building, but it has also required broader thinking about what they can do to manage the market in more open, transparent, and supportive ways.

“By the competitive nature of fundraising that we’ve created as funders, we made voluntary sector organisations just run around after money, and the government does the same: therefore we have to do something to make it easier, because the way it works now isn’t working.”

Grant Manager, independent foundation

A number of London-focused funders have been at the forefront of efforts to transform the capital’s funding environment, with the particular aim of promoting more giving. The City of London Corporation has been particularly active here, seeding initiatives such as City Philanthropy and Heart of the City that are aimed at strengthening philanthropy within the Square Mile. They have also provided funding to London Funders’ London’s Giving programme to expand the number of place-based giving schemes across the capital and embed a culture of giving at a local level (see General Public section).

London’s trusts and foundations are also investing more on capacity building in order to increase the resilience of civil society organisations to the challenges of the current funding environment. At a borough level, the Walcot Foundation has, for example, partnered with

Battersea Power Station Foundation to provide grant support in order to help strengthen the voluntary sector in Lambeth and Wandsworth. And at a pan-London level, City Bridge Trust has set up The Cornerstone Fund: this will provide funding for infrastructure organisations across the capital, who in turn can direct capacitybuilding support to local organisations. A number of funders have gone a step further and are actively trying to shift the balance of power in the funding environment, introducing more participatory approaches to grantmaking and philanthropy.

55 John Lyon’s Charity in particular has seeded local membership organisations known as Young People’s Foundations across seven of the boroughs in which it works. These aim to bid collectively for funding, and distribute money and capacity-building support on the basis of open dialogue with members (see Case Study 2). Trust for London have taken a slightly different tack with funding aimed at giving disadvantaged Londoners voice.

56

For many of those working within the grant-making sector, London-level work represents a leading edge of funder practice within the wider UK context.

“There are funders who are doing brilliant things, things like the Young People’s Foundations, the Poverty Profile, the Way Ahead. They’re doing provocative things, and it’s gone far beyond ‘here’s £10,000, go and do your project, send a monitoring report, and that’s it.”

Grant Manager, livery company

International Case Study 1: Vital Signs – Toronto

In 2001, Toronto-based community foundation Toronto Foundation launched its first Vital Signs report, a study of pressing social issues within its area of benefit. This has since become an annual initiative, providing a consolidated overview of the trends and issues affecting the quality of life for local citizens. 57 The report is intended to help direct the work of the Foundation, leverage additional philanthropic funding from individuals, corporates and government, and guide activity around identified social issues.

The Vital Signs model employs a range of annually updated indicators to track trends in need and quality of life in Toronto across 10 thematic areas including income & wealth, housing, public safety, arts & culture, and the environment. The authors collate findings from over 200 surveys and datasets into the compilation of the report, incorporating both qualitative and quantitative research. As well as updating standing metrics, each year the report identifies specific themes for a more detailed cross-issue analysis. The 2017/18 report applied an equality lens to its analysis, detailing the extent to which race, geography, income and gender effect the quality of life of Torontonians. 42

Vital Signs also helps raise the profile of organisations working to address issues raised within the report. Through the Community Knowledge Centre – a searchable resource hosted by the Toronto Foundation – readers of Toronto’s Vital Signs are able to search an online database of over 260 community organisations. This provides information on organisations’ mission statements, how they are responding to problems highlighted in Vital Signs, and ways to give. Readers of Vital Signs are also asked to engage in a “Vital Conversation” with peers, in which discussants are encouraged to share opinions of the report as well as their own ideas on how pressing local issues can be addressed.

An increasing number of community foundations in the UK and internationally (including East End Community Foundation) are adopting the approach pioneered in Toronto. In the UK, studies modelled on Vital Signs often include a survey of local residents to ensure that identified issues are grounded in community experience and opinion.

b. General public

Overview and trends

As we have seen, London is an important national and global centre of giving. But how does this translate into the giving of time and money by ordinary Londoners, both generally and to London causes in particular?

There are good reasons to think that ordinary Londoners might give generously. 59To begin with, London is a wealthy city. Greater wealth should feed through to a higher value of charitable donations. It also has a relatively large ethnic minority population with high levels of religiosity and research suggests that many migrant communities, especially religious ones, give generously. Research by the University of Manchester found that giving as a proportion of income was highest among Britons of Pakistani or Bangladeshi ethnicity, who gave 5.3 per cent of their monthly income compared to 1.7 per cent among white Britons. 60 National polling by the BBC and ComRes in 2014 found that giving was higher among religious people, with 78 per cent donating money to charity in the previous months compared to 67 per cent of atheists. 61

Finally, while London is often thought of as a transient, atomised city, the capital is in fact characterised by a relatively strong sense of belonging. Recent research by Centre for London has highlighted that identification with London is as strong now as it was 40 years ago, despite the share of Londoners born outside the capital having doubled. 62 Again, we might expect this to result in high levels of giving to London causes.

In some respects, the actual picture is a positive one. Londoners give an estimated £2bn a year to charity, equivalent to 20 per cent of the total value of UK donations. 63 The most recent edition of CAF’s annual giving report found that Londoners gave the highest mean monthly donation to charity at £58 (UK = £40), and the joint-highest 64 median donation at £20 (UK = £18). 65

Moreover, recent years have seen Londoners mobilised in huge numbers around specific fundraising and wider giving campaigns. This has been seen most vividly in response to the series of tragic events occurring over the spring and summer of 2017 in the capital – namely the four terrorist attacks in Westminster, London Bridge, Finsbury Park and Parsons Green; and the horrific fire at Grenfell Tower.

Clearly, these campaigns reached far beyond the capital, and this makes it difficult to untangle the contribution of Londoners from the generosity shown by people from across the UK. In the case of the terrorist attacks, the British Red Cross (in partnership with London Emergencies Trust) launched a national appeal – the UK Solidarity Fund – which also raised money for those affected by the attack in Manchester. 66 The approach in these cases, and for Grenfell, were themselves modelled on the London Bombings Relief Fund, set up in response to the 7/7 bombings in the apital, which was successful in raising and distributing £12m to support victims and their families. 67

For Grenfell, a number of different campaigns were established (see Case Study 1), raising £26.5 million in total by the end of January 2018. 68 Again, many of these campaigns (including the British Red Cross and the National Zakat Foundation) were national in scope; however, some firmly targeted Londoners. In particular, fundraising by the Evening Standard (London’s only mass-circulation daily paper) through its Dispossessed Fund (managed by London Community Foundation) – and by the locally based Kensington and Chelsea Foundation – collectively raised £13.6 million. (The Evening Standard Grenfell Campaign was one of a series of high-profile fundraising campaigns run by the paper.). While the money raised was substantial, this fails to fully capture the outpouring of support from the local community and from across the capital, with large numbers of individuals, community organisations, and faith groups coming to donate goods or volunteer time. The donation of goods reached such intensity that it quickly became a major logistical challenge for charities on the ground. The British Red Cross, for example, had to sort and distribute 211 tonnes of donations, although this ultimately helped raise a further £200,000 for the appeal. 69

As well as responding to moments of crisis and adversity, Londoners have shown a readiness to respond in large numbers to calls for volunteering support around major public events. In 2017, the World Athletics Championships came to the capital, with Team London recruiting and deploying some 4,000 volunteers to support athletes and spectators. 70 This had echoes of London’s watershed moment for volunteering – the London 2012 Olympic Games – in which 240,000 people applied to become one of 70,000 “Games Maker” volunteers. 71 While debates continue as to the long-term impact of the Games on volunteering (see Case Study 3), there is a broad consensus that it helped raise the visibility and profile of volunteering in the capital. 72

“The Olympics put the fun back into volunteering. And people valuing the volunteers and what they did was really good. If nothing else it was good publicity for volunteering.”

Volunteer Manager, infrastructure organisation

Case Study 3: The volunteering legacy of London 2012

A key question hanging over Londoners’ impressive mobilisation around major giving and volunteering events is whether that level of engagement is ever sustained. This has been an especially vexed question in relation to London 2012. While the Games engaged substantial numbers of people, seeded volunteering organisations like Team London and helped raise the profile of volunteering, many feel that it failed in its promise to “Inspire a Generation” by creating a sustained volunteering legacy.

In the immediate wake of the Games, two 2013 reports from the House of Commons and House of Lords voiced concern over prospects for a volunteering legacy, with the Commons report stating: “We are not convinced that as much as possible is being done to build a lasting volunteering legacy”. 73, 74 More recent research has suggested that these fears were correct, finding very limited and shortterm increases in volunteering engagement following the Games. 75 Many of the volunteering experts we spoke to as part of this research echoed these findings, voicing pessimism about any lasting legacy from the Games.

“I think Londoners thought that 2012 would come along, and suddenly we’d engage lots and lots of new people, which we did in 2012 […] I just don’t think that translated into anything after that.”

Chair, infrastructure organisation

Reasons given for the failure to achieve a lasting volunteering legacy include:

- Lack of clear objective-setting around the funding or delivery of a volunteering legacy. 76

- An overestimation of the number of first-time volunteers engaged by the Games. 77

-

A failure to engage existing infrastructure organisations in planning and delivering the volunteering legacy. 78, 76

As a consequence of these failings, comparative analysis with the Sydney Olympics concluded that in Sydney the Olympics “broadened the scope of volunteering in people’s minds, encouraging them to participate in episodic and event volunteering”, while in London, by contrast, “there was limited evidence of an increase in post-Games volunteering”. 72

A decline in giving?

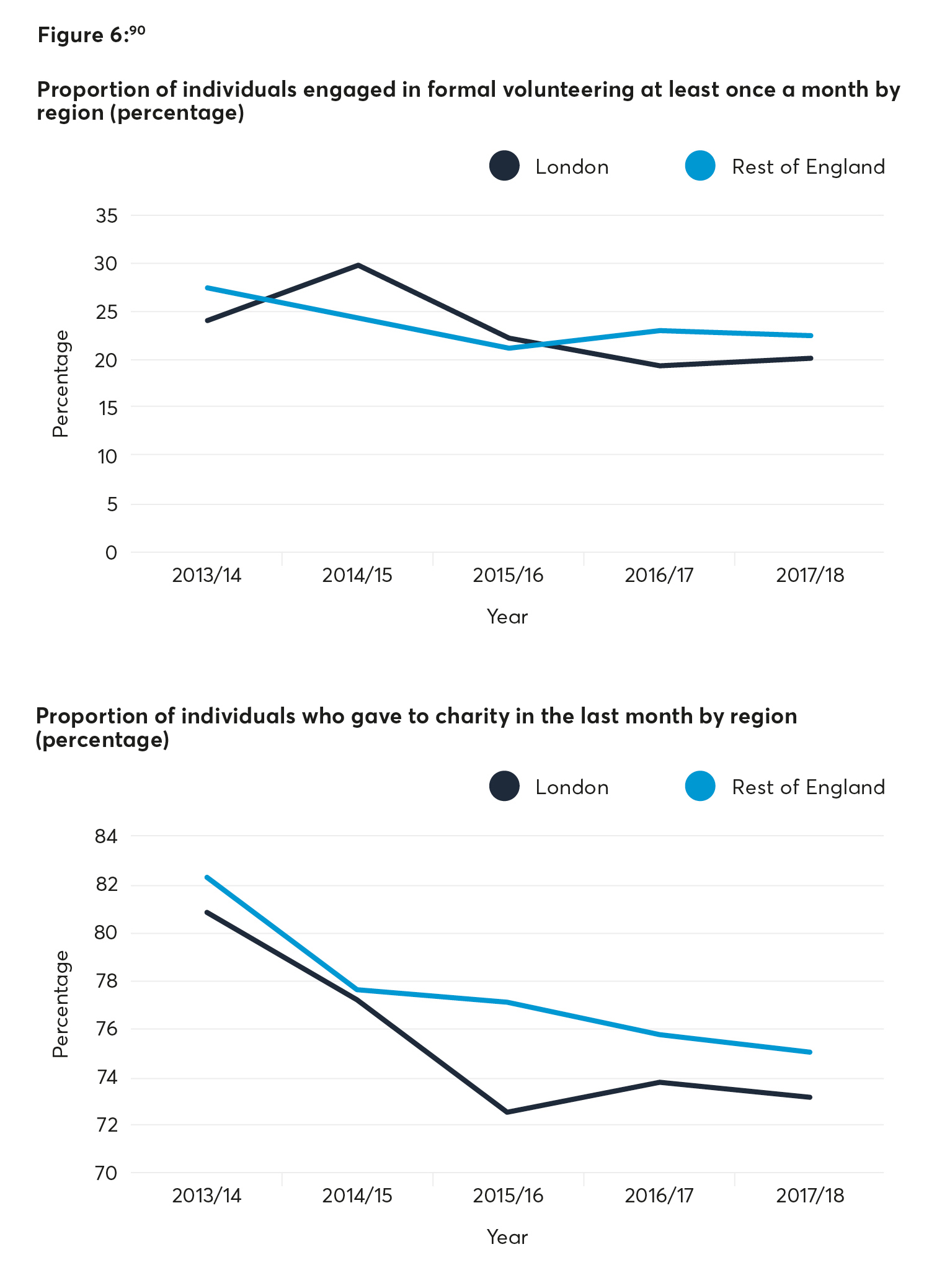

While individual Londoners are often generous, the big picture is by no means all positive. Surveys of giving habits have long shown that it is less common for Londoners than non Londoners to donate and volunteer regularly. But the same surveys also show falls in both regular donating and formal volunteering (defined as “providing unpaid help through groups, clubs or organisations”) by Londoners since 2013, when current data series begins. And while monetary giving and volunteering have fallen across the rest of England as well, the gap between monetary giving in London and the rest of England has widened – in 2013/14, 81 per cent of Londoners gave once a month but in 2017/18, only 73 per cent did (see Figure 6).

90: Official statistics from the Department for Culture, Media & Sport and Office for Civil Society Community Life Survey, 2013 to 2018. In 2016/17 the survey discontinued the face-to-face collection and moved fully to a self-completion online and paper mixed method approach.

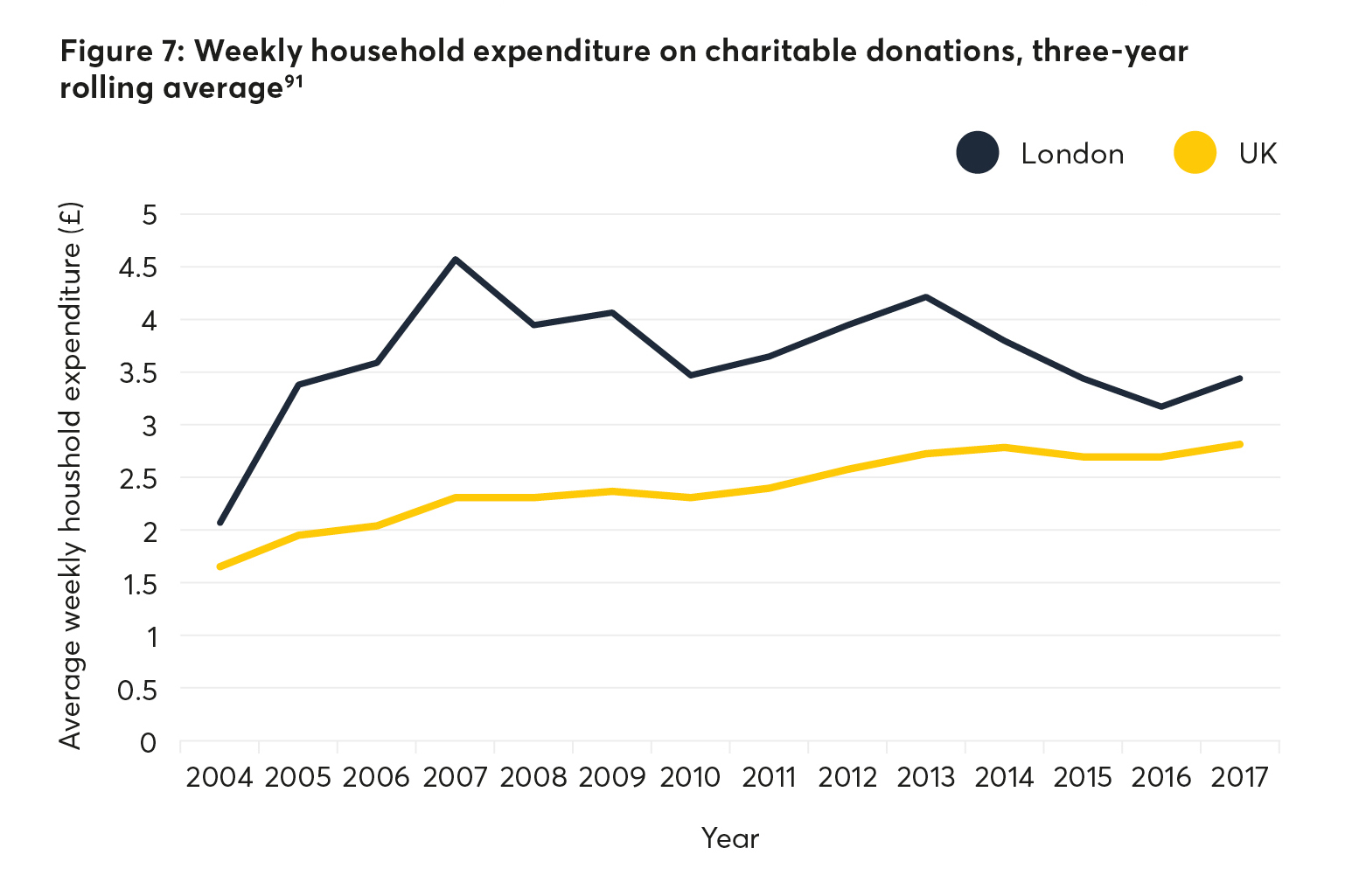

Moreover, though Londoners have long given more money on average to charity than non-Londoners (and still do), the gap has narrowed. A decade ago the average Londoner was giving twice as much to charity per week as the average UK person (London = £4.57 per week; UK = £2.30 per week). But this differential is now just 23 per cent (London = £3.43, UK = £2.80; see Figure 7).

91: Office for National Statistics (2018). Living Costs and Food Survey. London: Office for National Statistics.

Legacy giving

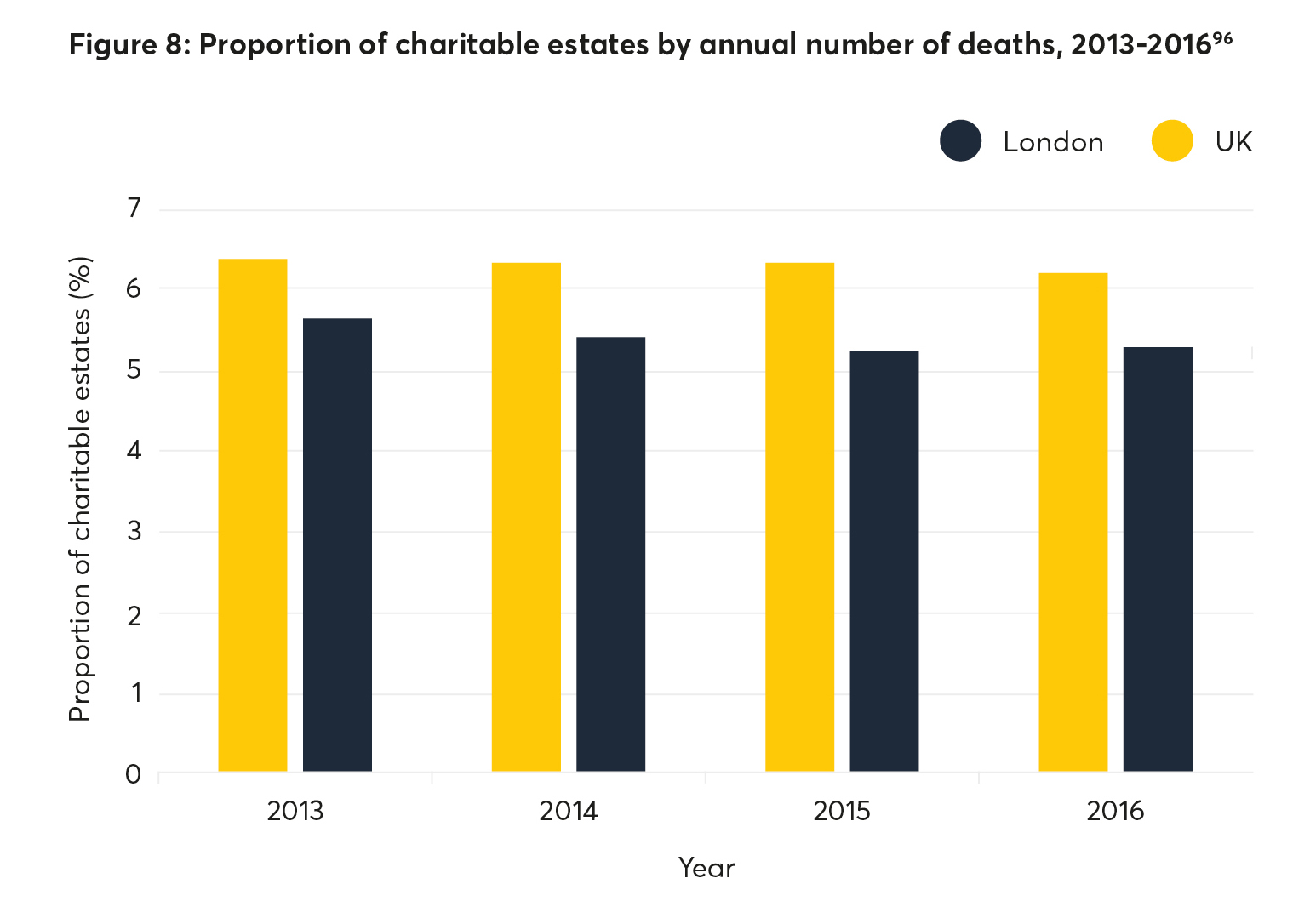

London also scores poorly when it comes to legacy giving. Across the UK as a whole, legacy giving remains stubbornly low, with just 7 per cent of people leaving a charitable bequest – a huge gulf when compared tothe proportion of people who say they give to charity in their lifetime. 81 But while participation in legacy giving is low across the country as a whole, it is lower still in London (see Figure 8). Only 5.3 per cent of Londoners who died in 2016 left a charitable bequest, 0.9 percentage points below the average for Britain. 82 What’s more, the potential for fundraising in London seems particularly high given the level of asset wealth locked up in housing.

Since 2009 house prices in the capital have risen by over 60 per cent, outstripping all other major towns and cities other than Cambridge. 83 Homes in Inner London are worth over 30 per cent more than all of the housing in Wales and Scotland put together, and Westminster and Kensington & Chelsea alone contain housing valued at £260bn. 84 If just a fraction of that asset wealth could be channelled towards legacies, the impact on the voluntary sector could be enormous.

96: Smee & Ford Legacy Research, Aug 2016.

96: Smee & Ford Legacy Research, Aug 2016.

London’s giving infrastructure

Volunteering

The landscape of advisory and infrastructure support for individual giving in London is complex, fragmented, and fast-changing. Infrastructure support for volunteering is arguably the most firmly established, with borough-level and pan-London organisations dedicated to encouraging the giving of time and matching volunteers to civil society needs.

Most boroughs will have some kind of volunteering support organisation tasked with helping local people find volunteering opportunities and supporting local charities to meet demand. The form and function of volunteer centres varies, however: 16 boroughs have an integrated volunteer centre and CVS, while 11 have an independent volunteering organisation. 85 There is also significant variability in the offer from different volunteer centres – some running their own volunteering programmes, others solely providing brokerage services, and still others only providing these services online. Research by Rocket Science reveals substantial variability in the resources available to local volunteer infrastructure organisations, with Newham’s volunteer centre receiving an income equivalent to one eleventh that of its counterpart in Sutton (£54,000pa vs £600,000pa). 42

At a pan-London level, the GLA has been active in promoting and facilitating volunteering through Team London. Team London provides brokerage services through its website and runs its own volunteering programmes – including provision of volunteer teams for major sporting events, training charity trustees, and programmes for certain beneficiary groups (e.g. Forces for London, focusing on employability outcomes for military veterans). A number of interviewees working at a borough level, however, spoke about a degree of wariness of Team London among some locally-based volunteering organisations, with Team London seen as “exclusive” and too focused on pursuing its own agenda – a wariness no doubt exacerbated by the funding squeeze on local organisations.

“It became more about Team London than it did about the groups on the ground. It felt like it was promoting Team London, promoting the GLA, but not promoting the groups on the ground.”

Director, volunteering organisation

However, the GLA seems alert to these issues and moves are now afoot to better coordinate and integrate Team London’s work with other London initiatives (see below).

There are also a variety of other organisations and networks supporting volunteering at different geographical scales and with different thematic priorities. Employee volunteering, in particular, is an area with a range of different organisations focused on supporting businesses (e.g. East London Business Alliance) and/or individual employees (e.g. BeyondMe) to access volunteering opportunities. (See the Corporates section for more detail). National and international volunteering organisations also operate across London, including Groundwork, which has an emphasis on green volunteering, and Hands On London, part of an international network of volunteering organisations providing opportunities for small community projects. Finally, there are a small number of active time banks in London, including Rushey Green and West Euston Time Banks, which provide opportunities for members to volunteer support.

London is always going to have a broad range of organisations promoting and supporting volunteering. But the large number we have identified raises the question of whether there is some opportunity for rationalisation. Our own research accords with those of the recent Way Ahead report: “[while] there are multiple routes to formal volunteering, [there is] no accessible route map for those searching for volunteering opportunities”. 87

Monetary giving

Monetary giving is most commonly driven by individual charities. There is limited organisation-level coordination between charities with respect to fundraising in London – although the Institute of Fundraising does connect individual fundraisers through its London and South East network group, and there are emerging examples of collaborative work between homelessness fundraisers (see Case Study 4).

Case Study 4: London Homeless Charities Group

With rough sleeping in London doubling since 2010, fundraisers at leading homeless charities developed an informal working group over 2016 and 2017 to share expertise and facilitate collaboration between charity fundraising teams. This forum ultimately grew to become the London Homeless Charities Group (LHCG), a coalition of 18 charities including St Mungo’s, Crisis, Shelter, Centrepoint, and Depaul – uniting behind a single campaign to raise funds for tackling rough sleeping in the capital. 88

In December 2017, LHCG partnered with the Mayor of London to launch the No One Needs to Sleep Rough in London campaign. 89 This joint initiative aimed to raise money for charities working with people sleeping rough, and develop awareness among the public about what they could do to help. It also aimed to raise awareness of new Mayoral policies designed to tackle the problem. As part of the campaign, a single donation point was set up for anyone looking to give towards rough sleeping prevention, with money raised being equally divided among the partner charities. In a traditionally competitive fundraising environment, this represents the first time that fundraising teams from homeless charities have joined forces to back a single campaign.

Despite limited time to develop the campaign, the first few weeks saw £85,000 raised from individual donations. While there is clearly scope to expand the reach and profile of the campaign and partnership, LHCG believes that it has established an approach that, with further development, has the potential to become a new model for fundraising in the homelessness sector. The group’s partnership with the GLA looks set to continue, and it is currently working to expand its fundraising activity to corporates, with the Mayor convening corporate partners to address rough sleeping in the capital.

It seems, unfortunately, that a number of giving campaigns within the capital have failed to “shift the dial” on individual giving. Most notably, the Penny for London initiative, which was launched in October 2014 by former Mayor Boris Johnson, hoped to raise £25 million

through encouraging Londoners to donate a penny every time they used their Oyster Cards. The scheme failed to engage a critical mass of Londoners (only 4,000 people signed up), and closed in August 2016 having raised just over £3,000.

90 Again, and despite some examples of coordination, there is probably opportunity to develop a much more strategic and collaborative approach to the promotion of monetary giving – especially where it concerns London causes.

International Case Study 2: Giving days – Washington, DC

Washington, DC has developed city-wide giving days as a way of driving citizen engagement in charitable giving and addressing need within the Washington, DC city region. 91 This began in 2011 with a one-off campaign, Give to the Max, and has run from 2013 onwards with the annual Do More 24 initiative, now in its fifth year. The current campaign is led by United Way NCA (part of the global United Way network of charities) and hosted online by a third party platform, which acts as a focal point for donations and as a directory of participating organisations.

Regional, national and local organisations with a presence in the Washington, DC area qualify to participate in the giving campaign. As well as an opportunity to raise cash and in-kind donations, the 24-hour giving event is recognised by its participants as an opportunity to increase awareness of social issues, raise their organisational profile, and grow their supporter base. While the Do More 24 initiative principally harnesses individual donations from members of the public, it also channels support from sponsorship and engages community and media partners. Deloitte, Goldman Sachs and Reed Smith are among the campaign’s lead sponsors.

During the giving day, participants can select the amount of money they would like to donate, and the organisation to which they would like the money to go. The event organisers have also created a prize system to spur both campaigning and giving. The prize structure awards additional monetary contributions to participating charities based on their success in raising their profile and donations. Prizes are awarded across a number of categories including size of organisation and impact on social media.

In its first year, the campaign raised over $1.3m in cash and in-kind donations for 500 participating organisations. In 2017, $1.67m was raised for 406 organisations, representing an absolute giving increase of 24 per cent in four years. 92

Giving infrastructure in flux: risks and opportunities for a step-change in giving by ordinary Londoners

The challenges of austerity and fragmentation have catalysed a significant response from within the sector – much of which has been driven by collaboration between GLV, the London Voluntary Service Council (LVSC), London Funders and City Bridge Trust around the Way Ahead Report. Following the publication of the report in 2016, a number of initiatives have been established that seek to rejuvenate local infrastructure. This includes City Bridge Trust’s Cornerstone Fund, which will provide £3m in additional funding to infrastructure organisations. Work is also currently underway to set up another key recommendation of the Way Ahead report – the London Plus. This will connect and strengthen local infrastructure across London (see Case Study 5). Both of these initiatives also have promise in bridging the divides between volunteering support organisations in the capital, with involvement from important stakeholders including the GLA/Team London and London Councils.

Alongside efforts to revitalise existing volunteering and wider civil society support organisations, a new infrastructure is emerging to encourage greater individual and corporate giving at a local level. This network of place-based giving schemes (PBGSs) has been inspired by the Islington Giving initiative, which was established by Cripplegate Foundation alongside other local and London-wide funders in 2010. Islington Giving aims to address inequality in the borough through a needs- and community-led approach, a core part of which involves growing the culture of giving in the local area. 93 So far Islington Giving has raised £6 million and engaged almost 5,000 volunteers: and the model is being replicated across the capital thanks to a programme of work by London Funders and City Bridge Trust. 94 Between 2014 and 2016 five new PBGSs were set up, collectively raising £4.3m. 95 At the time of writing, there are currently 11 active PBGSs in the capital.

While there are core principles underlying all PBGSs – including a commitment to collaborative working, a deliberative approach to establishing funding priorities, and a focus on promoting giving from local business and the community – the diversity of London’s boroughs means that PBGSs take quite different forms in each one. Southwark Giving, for example, has a strong focus on engaging the substantial number of corporates based in the borough, while Lewisham Local instead looks to encourage local community engagement from residents (including corporate employees who live in the borough).

“You mustn’t be jealous because the context is different. And the whole thing about place giving is actually it’s not about what you haven’t got, it’s about what you’ve got, and74 capitalising on what you have got. Don’t try and emulate because otherwise you’ll fall flat on your face.”

Director, local giving scheme

The differences between boroughs are also reflected in the makeup of partner organisations. In some boroughs PBGSs are “anchored” by a local grantmaking trust (e.g. Cripplegate in Islington and East End Community Foundation in Newham). However, in many other areas giving schemes don’t have grant-maker support, and this has made sustaining core costs a key challenge for many. While the PBGS model clearly has promise in stimulating a local giving culture, the issue of long-term sustainability represents the major obstacle to ensuring they become embedded features of local social infrastructure.

“The vision to have a giving model in each borough is a really good start. There’s potential there because people feel more passionate about what’s happening on their doorstep […] [but] a key question is how are they sustainable, because they just become a constant fundraising burden unless they’re endowed in some way. From a fundraising perspective it’s easy for fatigue to set in.”

Director, independent foundation

Case Study 5: London Plus

London Plus was a key outcome of the 2016 Way Ahead report, which recommended the creation of a pan-London infrastructure body to replace Greater London Volunteering (GLV) and the London Voluntary Service Council (LVSC). The Way Ahead set out a number of core functions for London Plus, including:

- A triage & connect role: diagnosing needs/issues of frontline volunteers and groups, and connecting these groups with support from civil society and business around knowledge, skills and resources.

-

Sharing data and gathering real-time intelligence: supporting the collation of pan-London data on need and civil society, as well as gathering and standardising need data from locally embedded organisations.

-

Campaigning for and catalysing change: providing a forum for a collective voice from infrastructure organisations, while also holding a mirror up to the sector and addressing poor practice.

Over 2017 and early 2018, GLV has led on developing London Plus, including setting up its steering group and terms of reference. The steering group has been established with a cross-sector membership, including representatives from London Councils and the GLA/Team London as well as private funders such as the Big Lottery and City Bridge Trust.

The development of London Plus is now focused around three core strands: data, networks, and voice & community. While still in its early stages, the ambition of London Plus is to act as a shared platform of support, enhancing intra- and inter-sectoral connections and maximising the assets of civil society – including the giving of time and skills by individual Londoners to support their communities.

c. Wealthy Londoners

Private wealth in London

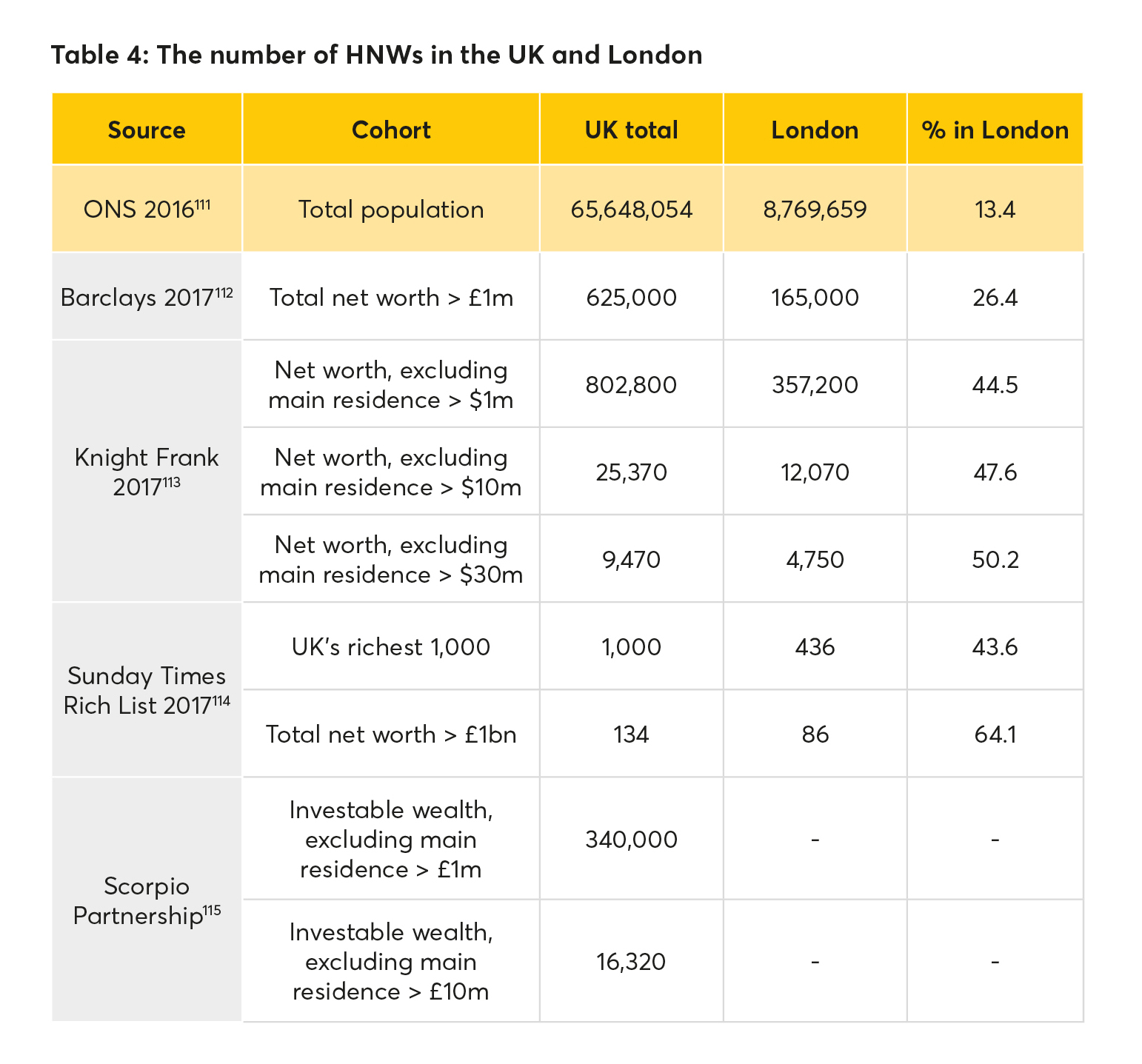

There is currently no commonly agreed metric for establishing, with any precision, the number, or national share, of “high net worth” individuals (HNWs) living in the capital. 96 But on any metric it is clear that London has a disproportionate share of the UK’s wealthiest. To take just one example, almost half the richest 1000 people in the UK (according the Sunday Times Rich List) live in the capital (see Table 4).

Comparative studies show that the capital also dominates on a global stage, with London having more billionaire residents than any other major city. 97 While this reflects a greater concentration of national wealth in the capital than many other Western nations, it also underlines the internationalism of London’s wealthy elite. Knight Frank’s 2016 wealth report found, for example, that seasonal flows of the wealthy in and out of the capital mean that London’s multi-millionaire population (resident in permanent or second homes in London) more than trebles over the course of a year, from a low of 10,000 in January to a peak of 35,000 in July. 98

111: ONS (2018). Population Estimates for UK, England and Wales, Scotland and Northern Ireland 2012-2016. Retrieved from: https://www.ons.gov.uk/peoplepopulationandcommunity/

populationandmigration/populationestimates/datasets/populationestimatesforukenglandandwalesscotlandandnorthernireland.

112: Barclays Wealth & Investments (2017). UK Prosperity Map 2017. Retrieved from: https://wealth.barclays.com/en_gb/home/research/research-centre/uk-prosperity-map.html.

113: Knight Frank (2017). The Wealth Report 2017. 11th Edition.

114: The Times (2017). The Sunday Times Rich List 2017.

115: Kail, A., Johnson, S., & Bowcock, M. (2016). Giving More and Better: How can the philanthropy sector improve? London: New Philanthropy Capital.

Research also suggests that the concentration of the very wealthy has grown in London, at least relative to the rest of the UK and almost certainly to the globe. According to the most recent Sunday Times Rich List, the number of billionaires in the UK has nearly doubled from 81 in 2008 to 145 in 2018, with the collective wealth of this group rising from £200bn in 2008 to £480bn over the same period. The capital is home to over 60 per cent (93) of all recorded billionaires in the UK, who hold over 70 per cent (£350bn) of the total wealth of UK billionaires. 99

At a London-wide level, Knight Frank finds that the number of ultra-high-net-worth individuals (>$30m in assets) rose by 41 per cent between 2005 and 2015, and predicts a continued increase of 30 per cent over the next decade. 100 And at the lower end of the HNW distribution, Barclays’ most recent UK Prosperity report finds that the number of London millionaires (though it does not define what it counts as a “millionaire”) rose by 6.5 per cent between 2016 and 2017. 101

Giving by London’s wealthiest

In many ways this concentration of wealth represents a major boon for giving in London. Over the ten years since Coutts have been running their annual Million Pound Donor Report (2008-2017), 72 per cent of alldonations 102 over £1m have come from the capital, totalling £9.77bn. 103 This broadly tallies with City Philanthropy’s estimate 104 for the value of major gifts from Londoners of £856m a year, equivalent to 15 per cent of cash giving in London. 105

While we have relatively strong data on major gifts from committed HNW philanthropists, little data is available on regular giving from the capital’s wealthiest residents. The Coutts figures, for example, while substantial in total value, relate to a relatively small number of individual donations. In the most recent annual figures (2017), Coutts recorded just 43 donations from individuals at a national level. General surveys of giving (e.g. CAF’s annual giving survey or ONS’ Living Costs and Food Survey) also fail to pick up the contribution of the very wealthy, who are too thinly distributed across the population to be included in survey samples.

Figures on regular giving are available at a national level, however, with wealth consultancy and research agency Scorpio Partnership estimating that average giving from individuals with an investable net worth of over £1m currently stands at £3,916 per year. 106 If we use the Barclays’ figures for the number of millionaires living in the capital (165,000), this gives an estimate for regular giving by HNW Londoners of £645 million per year. This estimate will include significant double counting with figures on major gifts. However, it is reasonable to assume that regular and major gift giving by HNWs in London lies somewhere in the region of £1bn to 1.5bn 107 annually.

Unengaged HNWs: average levels of giving remain low among the wealthy

For at least the last decade, research and commentary around HNW giving has regularly heralded a “new age of philanthropy” or a “boom time” for major giving.

108 This has been accompanied by the emergence of new terminology – such as “philanthrocapitalism” and

“philanthropreneurship” – signalling a modernisation and professionalisation of approaches to philanthropic giving. In particular, this involves applying business principles to the funding of social good.

109 The impact of austerity in London, and on the UK as a whole, has meant that giving from wealthy individuals has become an increasingly important part of the wider funding mix, with major donor fundraising one of the fastest-growing areas of UK charity fundraising practice.

110

Research into major gifts suggests that growing wealth has to some extent resulted in an increased number of large donations. The best evidence of this comes from Coutts’ national monitoring of donations over £1m, the number of which rose from 189 in 2006/7 to 310 in 2016. 103 This was driven by a rise in both unique and repeat donors (56 per cent and 71 per cent respectively) over this period – which suggests growing engagement with, and regularity of, major giving.

However, it is less clear whether growth in major gift giving has been reflected in shifts in the giving practices of most HNWs. Again, the best available data on this comes from national-level analysis. Research by Scorpio Partnership estimates that average giving by those with investable wealth of between £1m and £10m stands at £1,347 a year, while those with over £10m give £55,411 on average. 112 Scorpio Partnership estimates that this is equivalent to just 0.06 per cent of the total wealth of the £1-10m group, while those with over £10m fare little better at giving just 0.14 per cent of their total wealth. 113

The Philanthropy Collaborative (see Case Study 6) has calculated that the median level of giving among those with £1-10m in investable assets is just £500 a year. Among the ultra-wealthy – those with more than £10m – it is just £240. 114

Research on how the wealthy give also casts a somewhat negative light on HNW giving. Polling by NPC, for example, shows that high-income donors are more likely to give on an ad hoc basis (e.g. through one-off cash or credit card donations) than ordinary donors. 115

As already mentioned, these are national figures: it is possible that London’s wealthiest residents give somewhat more generously at a local level, encouraged, for instance, by the greater concentration of giving networks in the capital. However – anecdotally at least – many of our interviewees expressed dismay at what they saw as the disconnect between the wealth of many Londoners and their lack of engagement with philanthropy.

“London is one of the top five richest cities in the world, and, in that light, it is spectacularly unphilanthropic if I’m being brutal about it.”

CEO, charity

“It’s often very self-serving, and there’s lots more that individuals who are well off, particularly given the scale and size of bonuses […] could do, and it’s surprising that it doesn’t happen.”

Individual philanthropist

Which causes do London’s wealthy support?

Our knowledge of where giving by London’s wealthiest goes is also limited. At a national level, Coutts finds that the most common £1m+ donation between 2008 and 2017 was actually to other foundations. Once these gifts are removed from the overall total, we find that the most popular causes were higher education – with nearly half the value of all large donations (49 per cent) – followed by overseas organisations (14 per cent) and the arts (11 per cent). 116 Given that the vast majority of these gifts came from London-based donors, we can be reasonably confident that this distribution reflects giving in the capital.

Research by New Philanthropy Capital into the wider cohort of HNW individuals (defined in by the NPC study as individuals with annual incomes over £150,000) finds little contrast with the rest of the population, with both groups most likely to give to medical research (59 per cent high-income donors vs 49 per cent mainstream donors), hospitals and hospices (44 vs 45 per cent), and children and young people (46 vs 40 per cent). 115 High-income donors were, however, twice as likely to give to education and universities (24 vs 13 per cent) and the arts (14 vs 7 per cent) than mainstream donors.

HNW giving vehicles and advice in London

The concentration of wealth in London, combined with heightened visibility around philanthropy, has supported a growing constellation of organisations, networks, and platforms designed to encourage and facilitate giving by HNWs. For individuals and their families there are a broad range of organisations based in the capital that provide bespoke vehicles for giving, as well as wider philanthropy advice or education services. National organisations such as CAF and London’s community foundations (London Community Foundation and East End Community Foundation) facilitate giving from HNWs through a range of tailored structures and vehicles, including assistance with setting up and managing personal charitable trusts – often referred to as named or donor-advised funds (DAFs).

These vehicles enable donors to endow a fund with cash, shares or other assets in much the same way as setting up an independent foundation, but with fewer legal and administrative requirements (e.g. there is no requirement for a board of trustees). At a national level, there are currently £1bn worth of charitable assets managed through DAFs, which made grants of £280m in 2015/16. 118

Individual philanthropists can also seek support from a wider range of advisory and consultancy organisations based in the capital. This includes consultancies, such as New Philanthropy Capital and Ten Years’ Time, which provide bespoke guidance across the entirety of an individual’s “giving journey” – from establishing a causal focus to deepening subject knowledge and sector expertise, identifying promising ideas and delivery organisations, and understanding the impact of their giving on an ongoing basis.

There are also a growing number of organisations which aim to provide broader philanthropy education programmes to HNWs, including the London branch of The Philanthropy Workshop – an international network of philanthropists providing peer-based training around strategic approaches to giving. These organisations also include dedicated philanthropy centres at leading London universities (namely the Centre for Charitable Giving and Philanthropy at Cass Business School, and the newly established Marshall Institute at the LSE). As well as philanthropy specialists, professional service firms (e.g. financial advisors, accountants, wealth managers) can also play a key role in guiding and facilitating giving by HNWs – though research has shown that nationally just 1 in 5 wealth managers offer advice on philanthropy. 119

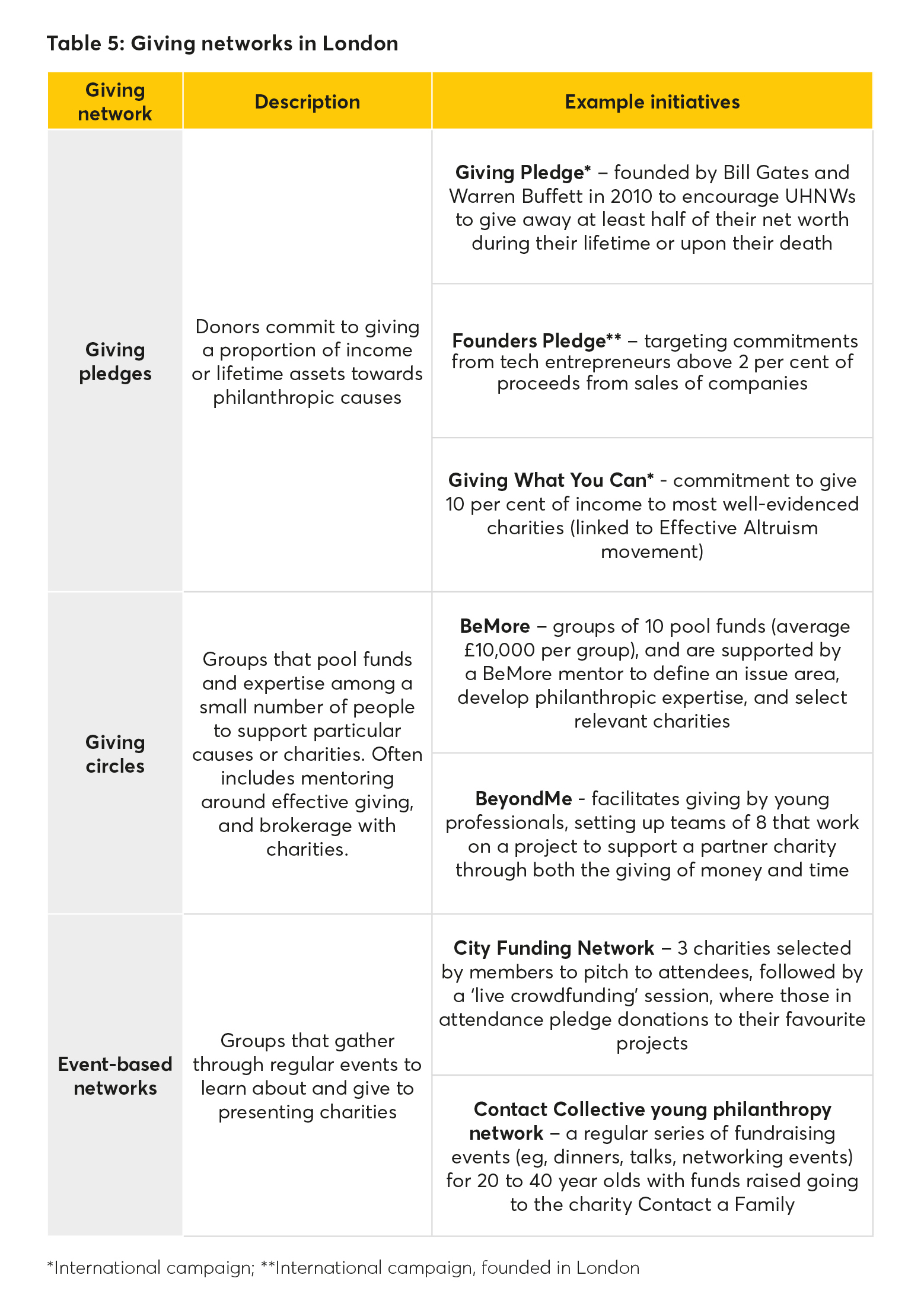

As well as support for individuals, London is home to a broad range of networks and groups that enable collective approaches to giving (see Table 5). These include giving campaigns that encourage wealthy individuals to pledge a certain amount of their income or assets; smaller giving circles, where members pool funds to support specific charities; and events that give charities and projects a platform to pitch for funding from attendees. There is significant variability in the level of wealth targeted by these initiatives, and hence their potential reach: the international Giving Pledge, for example, is focused on billionaires, while other initiatives aim to engage City graduates early in their careers. For this reason, some initiatives have significant blurring of edges with employee giving schemes (see the Corporates section).

Ideas and initiatives to support more and better HNW giving are also emerging from within philanthropic peer networks. Peer-led initiatives include the Philanthropy Collaborative, established in 2017, which aims to bring leading philanthropists and support organisations together to “normalise philanthropy among the wealthiest in Britain” and “generate an additional £2 billion per year of philanthropic giving” (see Case Study 6). 120 There has also been growing debate within the sector, encouraged in part by City Philanthropy, about whether to promote the idea of a City Bonus Pledge to increase giving among HNW Square Mile employees. This idea may well be gaining traction – with Rocket Science’s review of the City of London Corporation’s ongoing work to stimulate philanthropy in the Square Mile recommending a “market test [of] the viability of a bonus giving pledge from within the City’s financial/professional services sector”. 49

Case Study 6: The Philanthropy Collaborative

The Philanthropy Collaborative was formed in 2017 by the Hazelhurst Trust. This followed a 2016 report by New Philanthropy Capital, commissioned by the Trust, into how to increase the amount and effectiveness of giving from the philanthropy sector. 106 The Philanthropy Collaborative aims to take a philanthropist-led approach, bringing together committed HNW philanthropists to achieve the following goals: 123

-

Normalise philanthropy and social/impact investment among the wealthiest in Britain.

-

Generate an additional £2bn per year of philanthropic giving.

-

Generate additional private social and impact investment to make civil society more sustainable.

-

Develop a functioning, self-sustaining, cooperating ecosystem of philanthropy organisations.

-

Develop a stronger civil society coexisting with a vibrant economy that will be an exemplar for other countries.

To enable its collaborative approach the initiative will be run by a “philanthropists council”, supported by an administrative function, which will partner with other organisations to drive systemic change in five thematic areas: peer influence, public awareness, professional services, research and measurement, and political engagement.

Within each area, the council will commission a working group, bringing together expertise from across social and business sectors to address identified challenges. For example, within the peer influence area, this will include work to develop and expand co-funding networks and increase philanthropy education. For professional services, the Philanthropy Collaborative aims to increase philanthropy expertise among financial advisers and develop a directory of philanthropy advice.

Engaged HNWs: continued issues around transparency and collaboration

While questions remain about the aggregate contribution of HNWs in the capital, London undoubtedly has strong and growing networks of committed philanthropists. Those within the sector spoke about an increased willingness of individuals to take more strategic and evidence-based approaches in the capital, and to support a far larger range of causes than was the case 10 or 20 years ago.

“The scope of things that are supported has really expanded […] Back in the 80s it was all about art sponsorship and support […] but that effort now has really spread and expanded to include so many more dimensions of society, so you are seeing amazing philanthropists really supporting the broadest range of work you can imagine.”

Individual philanthropist

A key challenge remains, however: the lack of visibility and transparency around this kind of philanthropic giving. This in part reflects the challenges of monitoring individual donor practice, but it also results from a longstanding “culture of privacy and reticence about giving in the UK”, which is often contrasted with the far more public (self-) promotion of HNW giving in the US. 124 While some may caution the emulation of US approaches, a lack of openness in the UK can act as a barrier to charities and social enterprises accessing funding.

There is also substantial evidence that peer networks remain central to how many HNWs identify causes and organise their giving. The Richer Lives study, for example, found that the proportion of philanthropists who, when surveyed, said they had been influenced to give by someone they know (69 per cent) was more than double those who had been influenced by a professional fundraiser (31 per cent). 125 One downside is that organisations lacking contacts with often opaque personal philanthropic networks can find themselves shut out from an potentially vital source of funding.

“There doesn’t seem to be much of an escape from who knows who, and that’s a difficult gulf to bridge for small charities and their fundraisers.”

Individual philanthropist

The lack of transparency in giving and the importance of personal networks also have other potentially deleterious consequences. First, these factors can limit the levels of interaction and collaboration between individuals who sit within separate peer networks. For some, this has prevented the acknowledgement and wider engagement of certain groups of philanthropists, particularly those from ethnic minority backgrounds (see Case Study 7). This presents a major problem for individual HNW giving in London, and risks suppressing the high propensity to give within the capital’s BME communities.

“There needs to be greater celebration and recognition of [BME] people who are making these important contributions, and there are many, but you need to acknowledge that these are people who have been doing it for a while and it’s not brand new. It’s that acknowledgement that, it’s not because they haven’t done great things, it’s because they’ve been overlooked by the system.”

Individual philanthropist

Second, a lack of transparency and engagement beyond immediate networks may hinder the extent to which individual philanthropists collaborate with other actors in London’s wider funding ecosystem. In our interviews with practitioners from other sectors, we heard about a lack of engagement with HNW donors, and a sense that they operated within fundamentally different spheres. Again, there is a real risk of missed opportunities here, with cross-sector collaboration having the potential to combine the strengths of different actors. For example, the agility of individual actors can work powerfully with the evidence and resource base of grant-makers.

“The next key challenge is how you link some of the high-net-worth donors into those local groups as well. There needs to be a way of facilitating philanthropists to meet across the three main silos of trusts & foundations, corporates, and high value donors, and somehow getting those all talking.”

Grant Manager, independent foundation

Case Study 7: The Beacon Awards

The Beacon Awards are a biannual awards ceremony run by UK Community Foundations. Held in London but open to philanthropists from across the country, the awards aim to celebrate “pioneering approaches to giving”. The event aims to raise the profile of philanthropy and inspire others to become engaged in philanthropy or improve their giving practice. 126 The awards recognise good practice across a number of categories, including awards for City philanthropy (for philanthropists based in the Square Mile, Mayfair, or Canary Wharf), philanthropic innovation, impact investment, and partnership between a philanthropist and a charity.

For the 2017 edition, the Beacon Awards introduced a series of measures to ensure better representation of the diversity within the philanthropy sector (both demographic and disciplinary) than had been the case in previous years. To do this, organisers made a number of changes to key stages of the nominations and judging process, which included:

-

Nominations: The Beacon Awards partnered with other organisations to increase the diversity of its “nominees advisory panel” to access new networks and expand the pool of nominees. This included The Ubele Initiative – a social enterprise working with the African diaspora in the UK – who joined the nominees panel and provided additional advice.

-

Dissemination: Organisers also partnered with other organisations to promote the awards, in order to extend their profile and reach in soliciting nominations. This included partnering with the British Asian Trust to help promote the awards among philanthropists from the British Asian community.

-

Judging: New mechanisms were added to the judging process to ensure that the panel considered diversity throughout. Once provisional award winners had been decided, judging panel chairs met in order to review whether the awards were sufficiently representative.

-

Awards: New awards were added for the 2017 event. These included the Trailblazer Award to recognise emerging philanthropists, designed to spotlight younger philanthropists who had often been displaced in previous years by individuals with long-standing involvement in philanthropy.

d. Corporates

Sector overview

The latest statistics show that London is home to 1.1 million businesses, accounting for 19 per cent of all enterprises in the UK. The capital has a far greater business density than other regions of the UK, with 1,519 businesses per 10,000 people compared to a UK average of 1,069, and just 657 in the North East. 127 London also has a greater share of large employers, with 57 per cent of all employees in the capital working for firms with over 250 staff, compared to 47 per cent of employees across the UK as a whole. 128 London is, of course, at the centre of the UK’s financial sector, accounting for 51 per cent of the total UK financial and insurance sector output (GVA). 129 The sector makes up 16 per cent of London’s total GVA, far larger than is the case in any other UK region (the second-highest is Scotland at 6.5 per cent).

While data on businesses in London is plentiful, there is a lack of clarity on how the makeup of London’s economy feeds through into levels of corporate giving. This is in part due to the difficulty of geographically isolating the giving activity of businesses with national or international reach. However, transparency around corporate giving has also been hampered by the scrapping, in 2013, of legal requirements (set out in the 2006 Companies Act) for businesses to report all donations above £2,000. 130 Currently, the best aggregate data on corporate giving comes from CAF’s biannual Corporate Giving by the FTSE 100 report, which finds that donations by these firms at a national level stood at £1.9bn (or 2.3 per cent of pre-tax profits) in 2016. 131 CAF analysis shows that giving by these largest companies has actually fallen in recent years, by £655m (or 26 per cent) since 2013.

There is no publicly available data, however, on the contribution of London-based corporates to these national figures. Given what we know about the sectoral makeup of London’s economy we can, however, make some inferences. For example, three-quarters of the FTSE 100 financial service companies are based in the capital, and across this sector as a whole, the level of corporate donations has fallen by 19 per cent since 2009 (despite just a 3 per cent fall in revenue over this period). In contrast, over two-thirds of the UK’s consumer goods companies are based in London, and this sector has seen a corresponding increase in giving of 40 per cent (compared to a 13 per cent rise in revenue). Taking this sector-by-sector approach, we estimate that giving by London-based FTSE 100 companies stood at £850m in 2016. 132

This estimate should, however, be read with some caution. First, it only assesses giving from a narrow cohort of the largest businesses in the UK; and second, it may overestimate the London share of giving from these firms, most of which will raise money across regional offices as well as their London HQs. Separate analysis by City Philanthropy estimates corporate giving in London to be worth far less at £327m 105 (or 6 per cent of the total amount given across the capital) – although these figures themselves are based on a sample of just 159 businesses in the capital. 134

The landscape of corporate giving in London: Approaches and causes

Another issue with the above estimates is that they only assess the value of giving from corporate donations. These represent just one aspect of corporate philanthropy, which also encompasses grant-making from corporate foundations, corporate CSR programmes, and employee giving and volunteering. 135

Corporate foundations are, for example, a growing feature of London’s giving landscape, with more large corporates channelling their philanthropic activity through dedicated foundations. 136 Due to their legal separation, the engagement of parent businesses in the day-to-day running of their foundations can vary significantly. Some corporate foundations (such as Lloyds Bank Foundation) operate in very similar ways to independently endowed trusts, while others have much closer ties to business priorities. As of 2013, there were 140 corporate foundations in England and Wales, of which almost half were based in London. 42 According to their most up-to-date accounts, the foundations based in the capital donated nearly £180m in total to charitable causes across London, the UK and the world, which equated to two-thirds of the total given by the top 50 corporate trusts and foundations. 41

Many companies also act as a vehicle to support monetary giving and volunteering by individual employees. This includes supporting employees to give on a regular basis through payroll giving. Using HMRC’s national data, our calculations suggest an estimated 156,000 London employees gave a combined total of £24m through payroll giving in 2016/17. 139 The giving of time and skills is another crucial element of corporate giving. A recent study by City Philanthropy found that 39 per cent of all London employees volunteered (either on an ad hoc or regular basis), while those engaged in formal giving networks donated over 10,000 pro bono hours of work per year. 105 While there are a range of intermediary and brokerage organisations that support the giving of time by employees, many firms also run their own corporate CSR programmes, which draw on firms’ financial and fixed capital resources as well as their employee skills base to deliver social impact in local communities. It is worth noting that public sector employers also support employee volunteering: for example, the government allows all its staff three days of paid volunteering leave a year. Understanding the contribution of these interventions is difficult, and is exacerbated by wildly different levels of reporting among firms – which make comparisons and aggregate assessments all but impossible.

Limited publicly available data also makes it difficult to accurately characterise the causes supported by corporate giving activities. The giving priorities of major firms can change quite quickly, with many operating single- or multi-year corporate-charity partnerships, and causes or specific charities selected by senior managers or the wider workforce. We do know, however, that there has been a strong presence of corporate giving in the areas of education, skills, employability and social mobility in the capital. A 2013 study into corporate philanthropy in Canary Wharf by academics from Queen Mary University, for example, found that “the main thrust of the [CSR] work has been with younger people with a specific focus on education and training and access to employment”. 141 The focus on education and social mobility has in part been driven by a desire to better utilise existing employee competencies through skills-based volunteering, as well as longer-term business planning to support a pipeline of talent into specific industries or organisations.

Case Study 8: UBS and Hackney Bridge Academy

UBS is an international financial services firm based in the City of London, which

has supported education in nearby Hackney for over 15 years. In 2007, it helped set up the Bridge Academy, a secondary school in one of the most deprived parts of London. The partnership aims to reduce educational disadvantage for poorer schoolchildren, in terms of results and personal development as well as higher education access.

Between 2007 and 2014, 3,600 employees provided 37,500 hours of support, while UBS employees, clients and suppliers donated a further £1m. 142 Examples of support from UBS employees included maths lessons for GCSE students, careers assemblies, work experience placements, and university interview practice. 143

Infrastructure and advisory support

There are a broad range of London-based and Londonfocused advisory organisations which support businesses to do good, including London-focused organisations like Heart of the City, as well as national (e.g. Business in the Community) and internationally operating organisations (e.g. London Benchmarking Group).